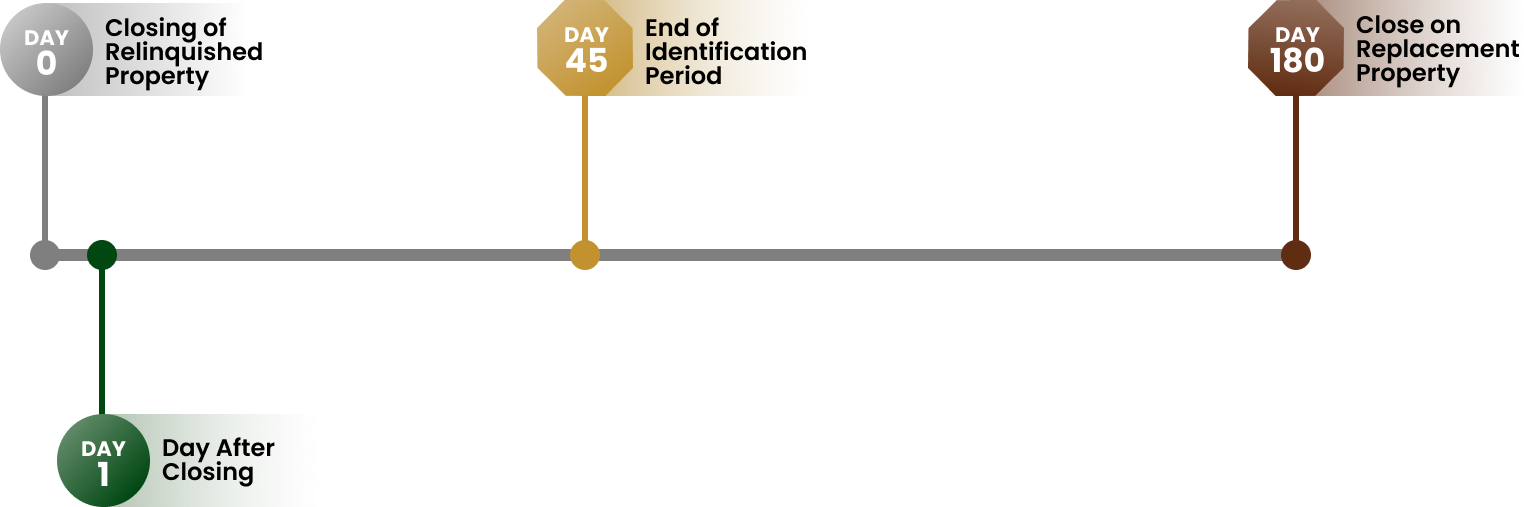

Timeframes

There are two timeframes to be aware of; the 45 day identification period and the 180 day exchange period.

Taxpayers have 45 calendar days after the transfer of their relinquished property to properly identify (customarily with the Qualified Intermediary) the exact property(ies) they intend to purchase through the 1031 transaction. This 45 day rule cannot be extended, even if it were to be on a weekend day or legal holiday.